In Canada, checking your credit score and credit report for free is a straightforward process managed by the two primary credit bureaus: Equifax Canada and TransUnion Canada. Fortunately, you can often do this without providing a credit card or SIN. The rise of trusted third-party services like Borrowell and Credit Karma has made it even simpler, offering instant access to your Equifax or TransUnion files with weekly updates and no negative impact on your score. Whether you're a first-time homebuyer in Toronto, a renter in Vancouver, or one of the many property managers in Alberta, understanding your credit score in Canada is critical for securing mortgages, loans, and rental agreements. This guide provides a comprehensive breakdown of how to check your credit score for free, highlights the key differences between Equifax and TransUnion, and offers actionable tips for maintaining a strong financial profile under the unique Canadian credit scoring system.

Your credit score plays a critical role in nearly every major financial decision you make in Canada, from renting an apartment to securing a mortgage or car loan. Yet many Canadians don’t fully understand how credit scores work, how they’re calculated, or how to check them without hurting their profile.

This guide breaks down what a credit score means in the Canadian context, how Equifax and TransUnion differ, how to check your credit score for free, and what steps you can take to improve or build credit from scratch. Whether you’re a renter, a newcomer to Canada, or planning your next big financial move, understanding your credit score is the first step toward better financial outcomes.

A credit score is a three-digit number, typically ranging from 300 to 900 in Canada, that summarizes your credit history and predicts your likelihood of repaying debt. It serves as a vital indicator of your financial health, profoundly influencing everything from mortgage approvals in Ontario to rental applications in Quebec. Lenders, insurers, landlords, and even some employers use your credit score to assess risk.

A higher score translates to better loan terms, lower interest rates, and a wider array of financial options. In the competitive Canadian real estate market, for example, property managers frequently run a credit check Canada before approving tenants. A strong score can unlock favorable rent payment plans or secure a lease with ease, while a low score may lead to rejection. Platforms like TenantPay, alongside other solutions, recognize the importance of reliable credit history for seamless financial integrations in property management.

Regularly monitoring your score helps you detect errors, potential fraud, or negative marks early, preventing costly surprises down the road. It's important to remember that unlike the U.S. system with its FICO scores, Canadian credit scoring depends on proprietary models from Equifax and TransUnion, which may not always be identical.

Canada’s bureaus translate detailed account data into a single number, but the underlying files reveal the nuance behind that score.

In Canada, your credit score is a dynamic number calculated from information in your credit bureaus report, which is a detailed record of your financial accounts, balances, and public records like bankruptcies. The score itself is a snapshot summary, while the report tells the full story. Both Equifax and TransUnion compile their reports by pulling data from banks, telecommunication companies, and utility providers.

For consumers with a limited Canadian credit history, often called "thin-file" consumers, scores might initially be lower, but they can be improved by cultivating responsible financial habits. A common misconception is confusing the credit score with the credit report: the report provides the detailed history, while the score offers a quick, analytical insight into your creditworthiness. Free access to your report is mandated, allowing you to see the details, while various free services provide the score for quick evaluations.

There are multiple no-cost routes to see your score and report without hurting your profile, from official bureaus to trusted fintech partners.

You can absolutely check your credit score for free. Both Equifax and TransUnion are required to provide free access to your credit report, and numerous online services now offer free scores as well. You can start with the official bureau portals by visiting their websites and entering personal details like your name, address, and birthdate.

In many cases, a SIN is not required for basic online access. If online verification is unsuccessful, phone and mail-in options are also available at no cost. For a more streamlined experience, third-party services provide comprehensive tools. Platforms like Borrowell deliver your full Equifax report and score in minutes, complete with weekly updates and fraud alerts, all without impacting your score.

Similarly, Credit Karma offers free TransUnion scores and monitoring. Even major banks like CIBC and Scotiabank now provide instant, free credit score access to their clients through their apps. A helpful tip is to request reports from both bureaus quarterly to check for discrepancies, as one might occasionally miss an update.

Below are fast, no-cost options you can use today.

Knowing how the two major bureaus differ helps you reconcile discrepancies and pick the right free monitoring tools.

When discussing credit bureaus in Canada, the comparison of Equifax vs Experian vs TransUnion is not entirely relevant, as Experian does not operate as a major consumer credit bureau here; its focus is primarily on the U.S. market.

The Canadian landscape is dominated by two main players: Equifax Canada and TransUnion Canada. These two entities act as the gatekeepers for nearly every credit check in Canada. When comparing Equifax and TransUnion, there are subtle differences. Equifax is known for updating its reports monthly and offers robust free online access, including scores provided through partners like Borrowell.

TransUnion provides free Consumer Disclosure reports but may charge for a score if requested directly, which is why free estimators or tools like Credit Karma are popular alternatives. The data itself can also vary, since a creditor might report to one bureau but not the other. This means a report from Equifax could show a more complete history for someone in British Columbia, while TransUnion might have more detailed data for a resident of Quebec. Neither bureau shares the "true" proprietary score that lenders use, but the free versions they provide are closely correlated and serve as excellent indicators of your financial standing.

To put your insights into action, understand the models used in Canada, what ranges lenders consider strong, and the habits that move the needle.

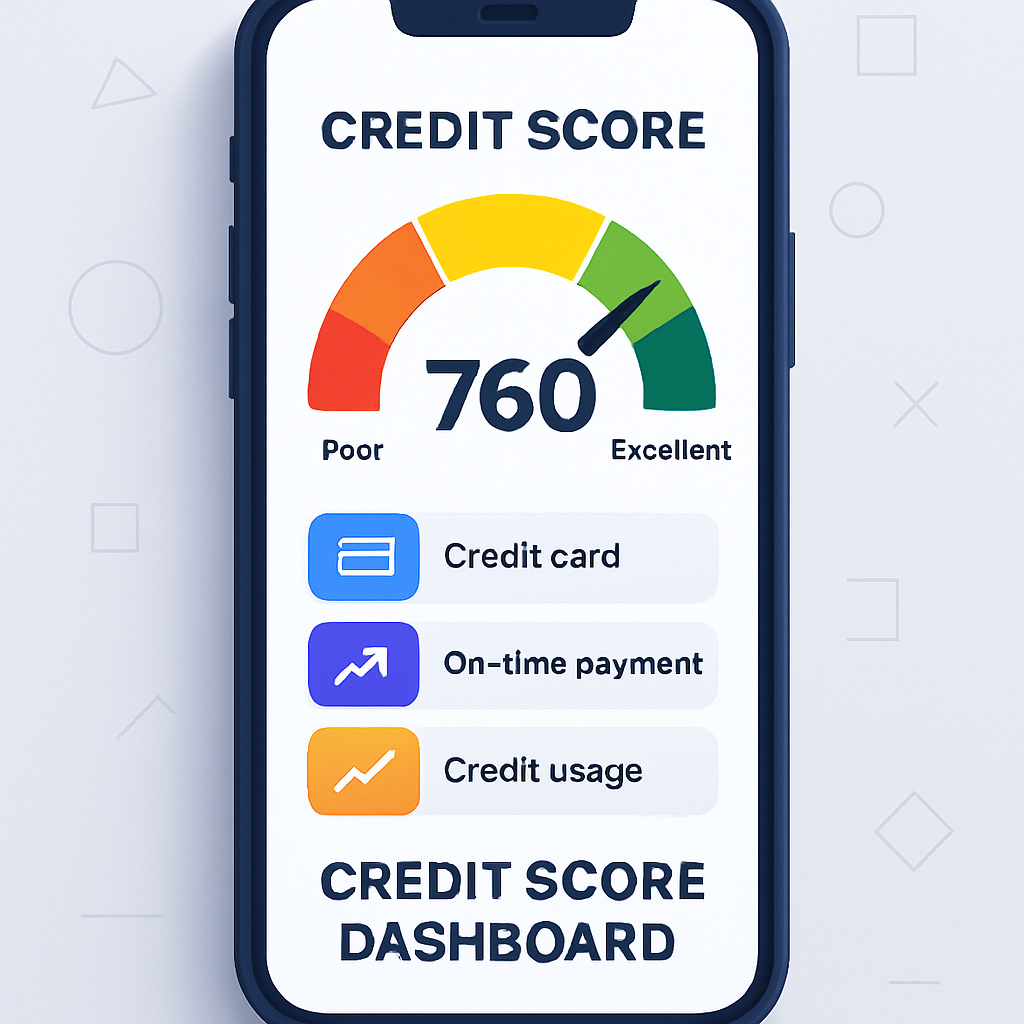

The concept of a FICO score Canada is a common point of confusion. FICO is a U.S.-centric credit scoring model, and Canada does not use the official FICO or VantageScore systems. Instead, Canadian bureaus utilize their own proprietary models, such as the Equifax Risk Score or TransUnion's own variant. While the names are different, the principles are similar: a good credit score in Canada generally falls between 660 and 724, with scores of 760 or higher considered excellent.

The debate of FICO vs VantageScore is therefore irrelevant in a Canadian context. It is more important to understand the factors that influence your score within the Canadian system. A significant development in this area is the rise of alternative data credit scoring, which uses information like rent payments or utility bills to help build a credit profile for no-file or thin-file consumers. This approach, which includes trended credit data, is particularly valuable for individuals new to Canada or those with limited credit experience.

In Canada, credit scores are generally categorized into ranges that signal your creditworthiness to lenders. A score between 660 and 724 is considered good, 725 to 759 is very good, and anything 760 or above is deemed excellent. Scores below 600 may result in denials for loans and credit products. An average score, such as 650, might qualify you for basic credit, but often at higher interest rates.

These ratings are consistent across the country, whether you're looking at credit score Ontario or credit score British Columbia, although lenders in competitive urban markets like Vancouver or Toronto might have higher benchmarks. Your score is not static; it is updated regularly, typically monthly by the bureaus, though services like Borrowell can provide weekly updates. The good news is that with dedication, you can improve your score over time.

Here are the core factors that influence your score in Canada.

Improving your credit score involves consistent, responsible financial behavior. The most effective strategies include always paying your bills on time, keeping your credit utilization low, and limiting the number of new credit applications you submit. If you're building your credit from scratch, a great starting point is to obtain a secured credit card, where you provide a deposit that typically matches your credit limit.

Another effective method is to become an authorized user on the credit card of a family member with a strong credit history. Furthermore, innovative services now allow you to report your rent payments to credit bureaus, which can significantly help unscored consumers build a positive file. For instance, TenantPay's rent reporting feature offers a powerful way to use your largest monthly expense to your advantage and establish a strong credit foundation. For those looking to secure a loan, aiming for a credit score of 660 or higher is recommended, with scores over 720 being optimal for securing the best interest rates.

Checking your good credit score in Canada is free, easy, and essential for making informed financial decisions, from securing a rental in Quebec to obtaining a mortgage anywhere in the country. By leveraging the free resources provided by Equifax, TransUnion, and trusted services like Borrowell and Credit Karma, you can stay vigilant, build positive financial habits, and unlock new opportunities. For property managers and landlords, understanding these tools ensures that tenant screenings are fair and effective, while integrating modern payment platforms helps maintain a seamless and reliable rental operation.

A good credit score in Canada is between 660 and 724. A score of 725 to 759 is considered very good, and 760 or higher is excellent, giving you access to the best interest rates.

You can get a free credit score and report from services like Borrowell (Equifax) and Credit Karma (TransUnion) or directly from the credit bureaus online. Many Canadian banks also offer this feature to their clients for free.

A credit score is a three-digit number between 300 and 900 that summarizes your credit history and helps lenders assess the risk of lending you money.

To improve your score, focus on paying all your bills on time, keeping your credit card balances below 30% of your limit, and avoiding too many credit applications in a short period.

Your credit score impacts your ability to get approved for loans, mortgages, and even rental applications. A higher score often leads to better interest rates and more financial opportunities.

No, Canada does not use the FICO score. The main credit bureaus, Equifax and TransUnion, use their own proprietary scoring models to evaluate creditworthiness.

Credit bureaus typically update your score monthly. However, free monitoring services like Borrowell or Credit Karma can provide weekly updates.

The most important factors are your payment history, how much credit you are using (credit utilization), the length of your credit history, the types of credit you have, and recent credit inquiries.

A score of 650 is considered fair or average. It may be sufficient to qualify for some credit products, but you will likely face higher interest rates. Aiming for a score above 660 is recommended.

Yes. You can start by getting a secured credit card, becoming an authorized user on someone else's card, or using services that report your rent payments to the credit bureaus.